When considering a loan, one of the most important decisions you’ll face is choosing between a secured loan and an unsecured loan. Both types of loans can help you meet financial goals such as buying a home, funding education, consolidating debt, covering emergency expenses, or financing a major purchase. However, they differ significantly in terms of collateral requirements, interest rates, approval criteria, and risk.

Understanding the differences between secured and unsecured loans can help you make an informed borrowing decision and choose the option that best fits your financial situation.

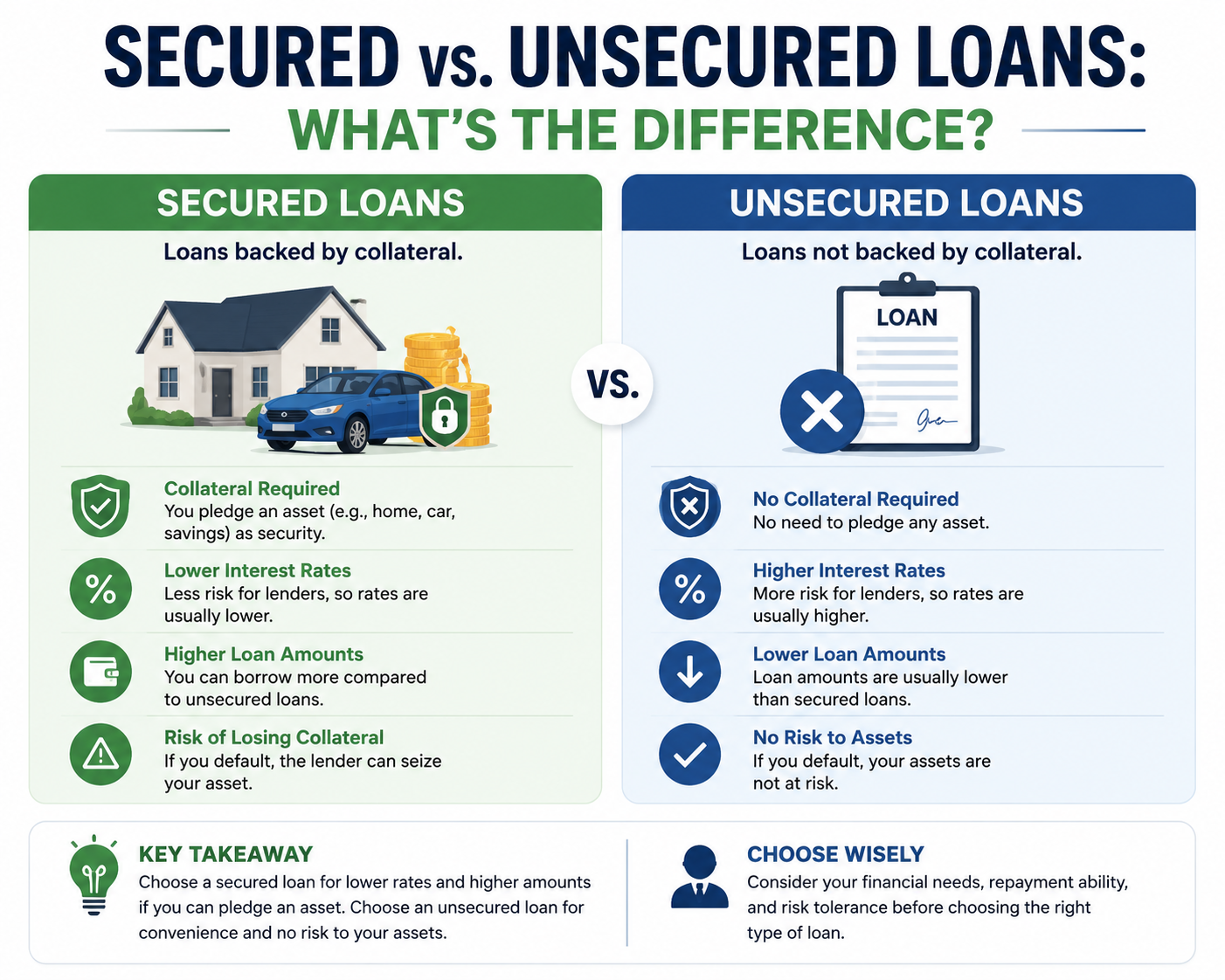

What Is a Secured Loan?

A secured loan is a type of loan that requires the borrower to provide an asset as collateral. The collateral serves as security for the lender, reducing the risk associated with lending money.

Common forms of collateral include:

- Real estate property

- Vehicles

- Fixed deposits

- Savings accounts

- Investments

- Valuable assets

If the borrower fails to repay the loan according to the agreed terms, the lender has the legal right to seize the collateral to recover the outstanding debt.

Examples of Secured Loans

Some common examples of secured loans include:

- Home loans (mortgages)

- Auto loans

- Loan against property

- Gold loans

- Secured personal loans

- Loans against fixed deposits

Because collateral reduces lender risk, secured loans often come with more favorable terms compared to unsecured loans.

Advantages of Secured Loans

Lower Interest Rates

One of the biggest benefits of secured loans is lower interest rates. Since the lender has collateral as security, they are willing to offer more competitive rates.

Higher Loan Amounts

Secured loans generally allow borrowers to access larger amounts of money because the lender’s risk is minimized.

Easier Approval

Borrowers with average or poor credit scores may find it easier to qualify for secured loans since collateral provides additional protection for the lender.

Longer Repayment Terms

Many secured loans offer extended repayment periods, making monthly installments more manageable.

Disadvantages of Secured Loans

Risk of Losing Assets

The biggest drawback is the possibility of losing your collateral if you fail to make payments.

Longer Approval Process

Secured loans often require asset verification, valuation, and additional documentation, which can slow down approval.

Limited Flexibility

The loan amount may depend on the value of the collateral rather than your actual financial needs.

What Is an Unsecured Loan?

An unsecured loan does not require any collateral. Instead, lenders approve borrowers based on factors such as:

- Credit score

- Income level

- Employment history

- Debt-to-income ratio

- Financial stability

Because there is no collateral involved, the lender assumes greater risk when approving the loan.

Examples of Unsecured Loans

Common unsecured loans include:

- Personal loans

- Credit cards

- Student loans

- Medical loans

- Small business loans (in some cases)

These loans are popular because they provide access to funds without requiring borrowers to pledge personal assets.

Advantages of Unsecured Loans

No Collateral Required

The most significant benefit is that borrowers do not risk losing valuable assets if financial difficulties arise.

Faster Approval Process

Since there is no collateral evaluation, unsecured loans often have quicker approval and funding times.

Greater Flexibility

Borrowers can typically use unsecured loan funds for various purposes without restrictions.

Simple Documentation

Many unsecured loan applications require less paperwork compared to secured loans.

Disadvantages of Unsecured Loans

Higher Interest Rates

Because lenders face greater risk, unsecured loans generally carry higher interest rates.

Stricter Eligibility Requirements

Borrowers usually need stronger credit profiles and stable income to qualify.

Lower Loan Amounts

Without collateral, lenders may limit the amount they are willing to lend.

Shorter Repayment Terms

Some unsecured loans require repayment within a shorter timeframe, leading to higher monthly payments.

Secured vs. Unsecured Loans: Key Differences

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral Required | Yes | No |

| Interest Rates | Usually Lower | Usually Higher |

| Approval Difficulty | Easier for some borrowers | More dependent on credit profile |

| Loan Amount | Higher | Lower |

| Approval Speed | Slower | Faster |

| Risk to Borrower | Loss of collateral possible | No asset risk |

| Credit Score Importance | Moderate | High |

| Repayment Terms | Often Longer | Often Shorter |

Which Loan Type Is Right for You?

The best choice depends on your financial goals, credit profile, and risk tolerance.

Choose a Secured Loan If:

- You need a large loan amount.

- You want lower interest rates.

- You have valuable collateral available.

- Your credit score is less than ideal.

- You are comfortable pledging an asset.

Choose an Unsecured Loan If:

- You don’t want to risk personal assets.

- You need quick approval.

- You have a good credit score.

- You require a smaller loan amount.

- You prefer a simple application process.

Factors to Consider Before Applying

Regardless of the loan type you choose, evaluate the following:

Monthly Affordability

Ensure that loan payments fit comfortably within your budget.

Total Cost of Borrowing

Look beyond monthly payments and calculate the total interest and fees you’ll pay over the loan term.

Loan Purpose

Match the loan type to your financial need. Large purchases often suit secured loans, while smaller expenses may be better handled through unsecured loans.

Financial Stability

Consider your income stability and ability to maintain regular repayments.

Common Mistakes Borrowers Make

Many borrowers rush into loan decisions without fully understanding the consequences.

Avoid these common mistakes:

- Borrowing more than necessary

- Ignoring loan terms and conditions

- Focusing only on monthly payments

- Not comparing multiple lenders

- Using secured loans for unnecessary expenses

- Missing repayment deadlines

Careful planning can help prevent financial stress and costly mistakes.

Conclusion

Both secured and unsecured loans offer valuable financing solutions, but they serve different purposes and come with unique advantages and risks. Secured loans provide lower interest rates, higher borrowing limits, and easier approval for some borrowers, but they require collateral and carry the risk of asset loss. Unsecured loans offer convenience, speed, and flexibility without putting personal assets at risk, though they often come with higher interest rates and stricter approval requirements.

Before choosing a loan, carefully assess your financial needs, repayment ability, credit profile, and comfort level with risk. Comparing multiple loan options and understanding the full terms of the agreement can help you make a confident decision that supports your long-term financial well-being. The right loan is not simply the easiest one to obtain—it’s the one that aligns with your financial goals while remaining affordable and manageable throughout the repayment period.