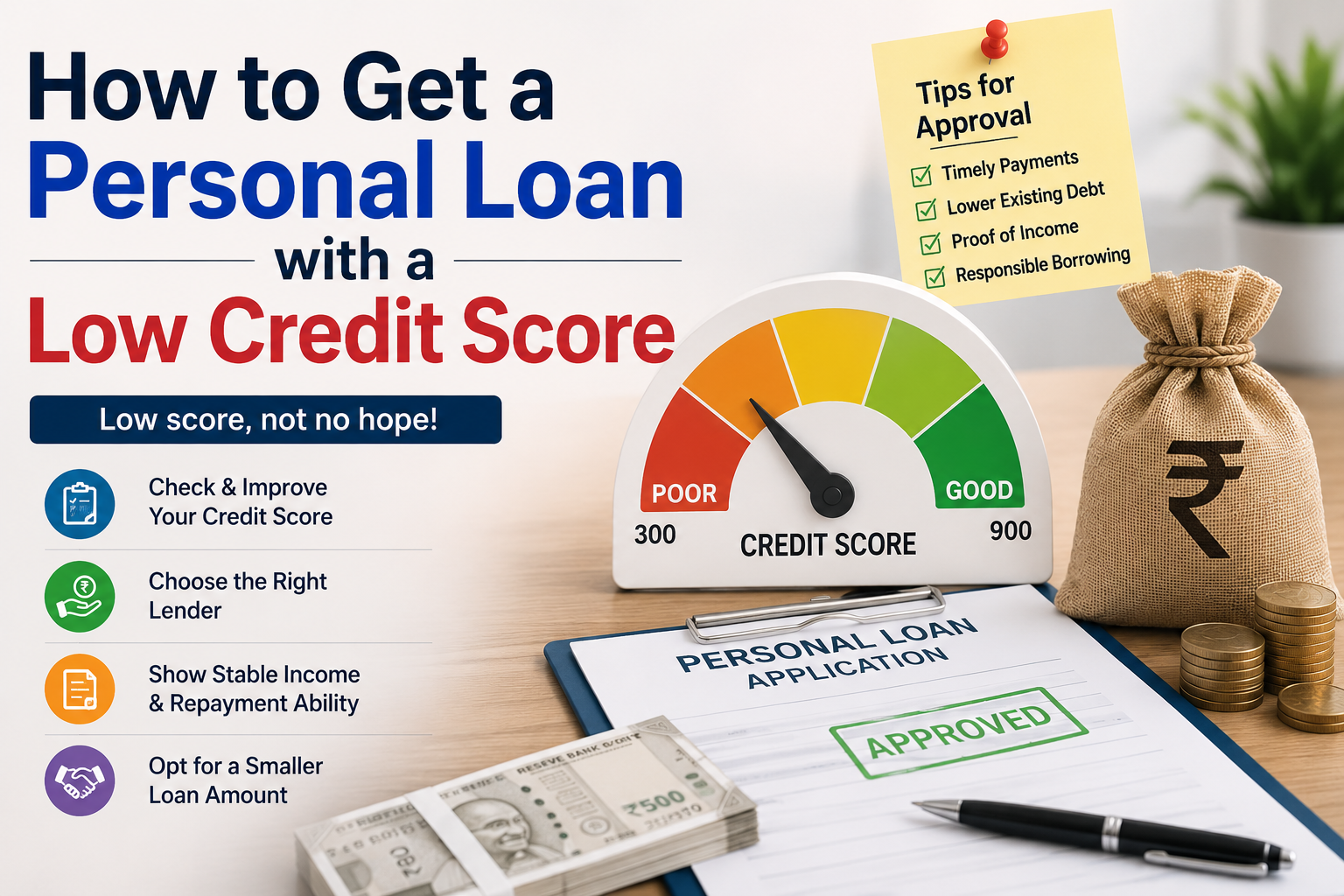

Getting approved for a personal loan can be challenging when you have a low credit score, but it is far from impossible. Many lenders understand that credit scores do not always tell the complete story of a person’s financial situation. Whether your credit score has been affected by missed payments, financial hardships, or limited credit history, there are still ways to secure a personal loan and access the funds you need.

In this guide, we’ll explore practical strategies that can improve your chances of getting a personal loan with a low credit score and help you make informed borrowing decisions.

Understanding Low Credit Scores

A credit score is a numerical representation of your creditworthiness based on your borrowing and repayment history. Lenders use this score to assess the risk of lending money to you.

Generally, a lower credit score may indicate:

- Missed or late payments

- High credit card balances

- Loan defaults

- Bankruptcy history

- Limited credit history

Because lenders view low credit scores as a higher risk, borrowers may face higher interest rates, stricter approval requirements, or lower loan amounts.

However, having a low credit score does not automatically mean your loan application will be rejected.

Can You Get a Personal Loan with Bad Credit?

Yes, many lenders offer personal loans specifically designed for individuals with poor or fair credit. These lenders often evaluate additional factors beyond your credit score, such as:

- Monthly income

- Employment stability

- Debt-to-income ratio

- Banking history

- Current financial obligations

Demonstrating financial responsibility in these areas can significantly improve your approval chances.

Steps to Improve Your Chances of Loan Approval

1. Check Your Credit Report First

Before applying for a loan, review your credit report carefully. Errors on credit reports are more common than many people realize.

Look for:

- Incorrect account balances

- Duplicate accounts

- Fraudulent activity

- Incorrect payment records

Correcting these errors could improve your credit score and increase your eligibility for better loan terms.

2. Improve Your Debt-to-Income Ratio

Lenders want to know that you can comfortably manage additional debt.

Your debt-to-income (DTI) ratio compares your monthly debt payments to your monthly income. A lower DTI ratio demonstrates better financial stability.

To improve your DTI:

- Pay down existing debt

- Avoid taking on new debt

- Increase your income if possible

Even small improvements can strengthen your loan application.

3. Apply for the Right Loan Amount

One common mistake borrowers make is requesting more money than they actually need.

Lenders may be more willing to approve smaller loan amounts because they represent lower risk. Borrowing only what is necessary can increase your chances of approval and reduce your overall repayment burden.

4. Show Proof of Stable Income

A steady income is one of the most important factors lenders consider.

Documents that may help verify your income include:

- Salary slips

- Bank statements

- Tax returns

- Employment verification letters

A stable income reassures lenders that you can make regular loan payments, even if your credit score is lower than ideal.

5. Consider a Co-Signer

If possible, applying with a co-signer can significantly improve your approval odds.

A co-signer agrees to take responsibility for the loan if you fail to make payments. Because the lender can also rely on the co-signer’s creditworthiness, they may offer better interest rates and loan terms.

However, both parties should understand the financial responsibilities involved before entering into a co-signing agreement.

6. Explore Secured Loan Options

Secured loans require collateral, such as:

- A vehicle

- Savings account

- Fixed deposit

- Property

Providing collateral reduces the lender’s risk and can improve your chances of approval despite a low credit score.

Keep in mind that failing to repay a secured loan could result in the loss of the pledged asset.

Avoid Common Loan Application Mistakes

When applying for a personal loan, avoid these common errors:

Applying to Too Many Lenders

Submitting multiple loan applications in a short period can negatively impact your credit profile and make lenders cautious.

Ignoring Loan Terms

Always review the loan agreement carefully. Pay attention to:

- Interest rates

- Processing fees

- Late payment penalties

- Repayment schedule

Borrowing More Than You Can Afford

Just because you’re approved for a certain amount doesn’t mean you should borrow the maximum available. Ensure the monthly payments fit comfortably within your budget.

Tips for Managing Your Loan Successfully

Once approved, responsible repayment is essential.

To stay on track:

- Set up automatic payments

- Pay installments on time

- Create a monthly budget

- Avoid taking on additional debt

- Monitor your credit score regularly

Consistent on-time payments can gradually improve your credit score and open the door to better financial opportunities in the future.

Alternatives to Personal Loans

If you’re struggling to qualify for a personal loan, consider alternative options such as:

- Credit union loans

- Secured loans

- Family or friend loans

- Employer salary advances

- Debt management programs

These alternatives may provide more affordable financing depending on your circumstances.

Conclusion

Getting a personal loan with a low credit score may require extra effort, but it is certainly achievable. By reviewing your credit report, reducing existing debt, demonstrating stable income, and choosing the right lender, you can improve your chances of approval and secure the funds you need.